For a bank using the advanced measurement approach to measuring operational risk, which of the following brings the greatest 'model risk' to its estimates:

A long position in a creditsensitive bond can be synthetically replicated using:

Which of the following is not a permitted approach under Basel II for calculating operational riskcapital

For a given mean, which distribution would you prefer for frequency modeling where operational risk events are considered dependent, or in other words are seen as clustering together (as opposed to being independent)?

Which of the following contributed to the systemic failure during the credit crisis that began in 2007?

As opposed to traditional accounting based measures, risk adjusted performance measures use which of the following approaches to measure performance:

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving thereturns of the S&P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month's payments, the bank enters bankruptcy. What is the legal claim thatthe hedge fund has against the bank in the bankruptcy court?

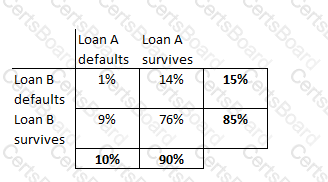

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. Theprobability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Which of the following is not an approach proposed by the Basel II framework to compute operational riskcapital?

TESTED 09 Apr 2026